What if the future for the U.S. economy is a hybrid of stagnant GDP growth, and dramatically higher wage inflation? I am not an economist and I am reluctant to propose this, but is it possible we will have low growth in real GDP but lingering inflation?

I have to keep reminding myself about how you score growth in an inflationary period – it is “real” revenues (based on units), not nominal revenues (headline number), that truly measure GDP growth. Units can go down, but reported sales and earnings can rise if prices increases are passed on to the customer.

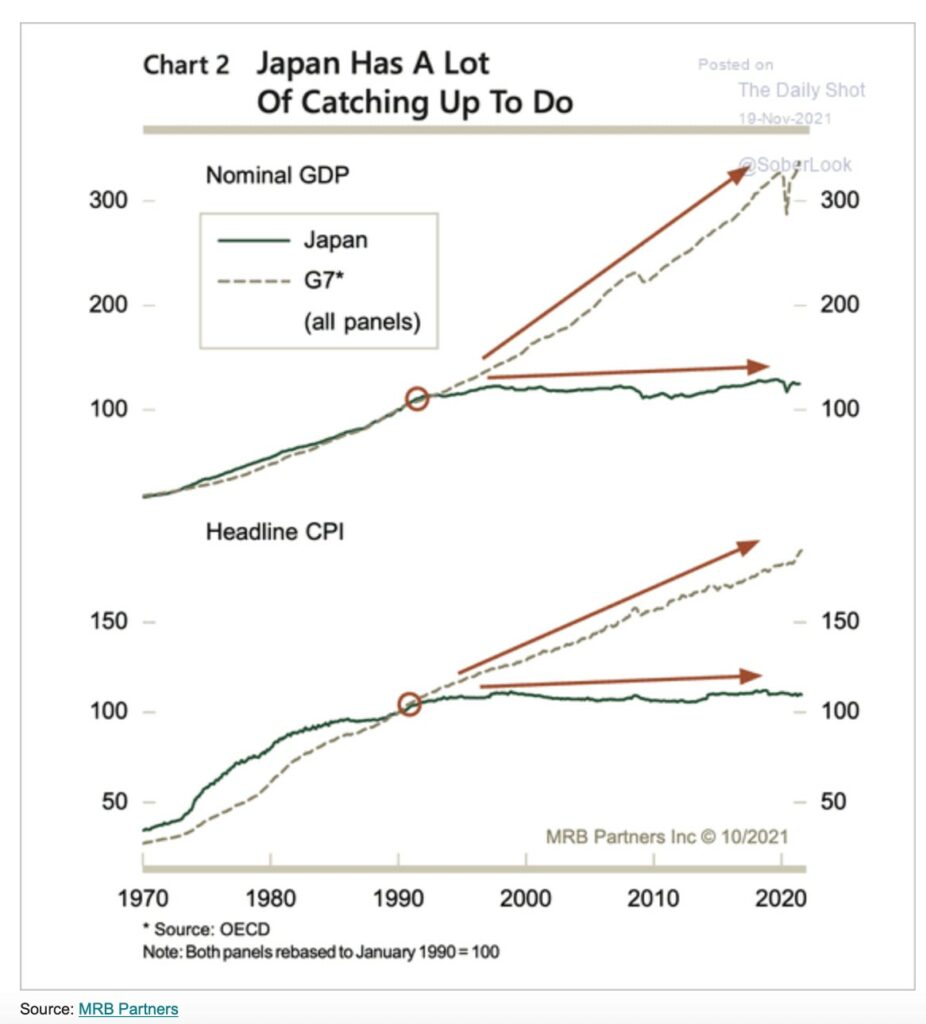

Japan Got Old First

I have been perplexed by the lack of GDP growth in Japan since its real estate and stock markets crashed in the early 1990’s, and it has an economy where nominal and real GDP are the same at just around 1%. It also has low interest rates and a liquidity underwriter in The Bank of Japan so it isn’t lack of capital.

It also has some of the highest savings per capita in the world.

Notwithstanding repeated attempts by BOJ to get retirees to spend, nothing has happened for 30 years. Why is this? My guess is the Japanese “retirement mind” and “working mind” are astoundingly different when it comes to spending habits, but that is just a guess. Demographics and changing mindsets may prove to be more persuasive than central bank accommodations?

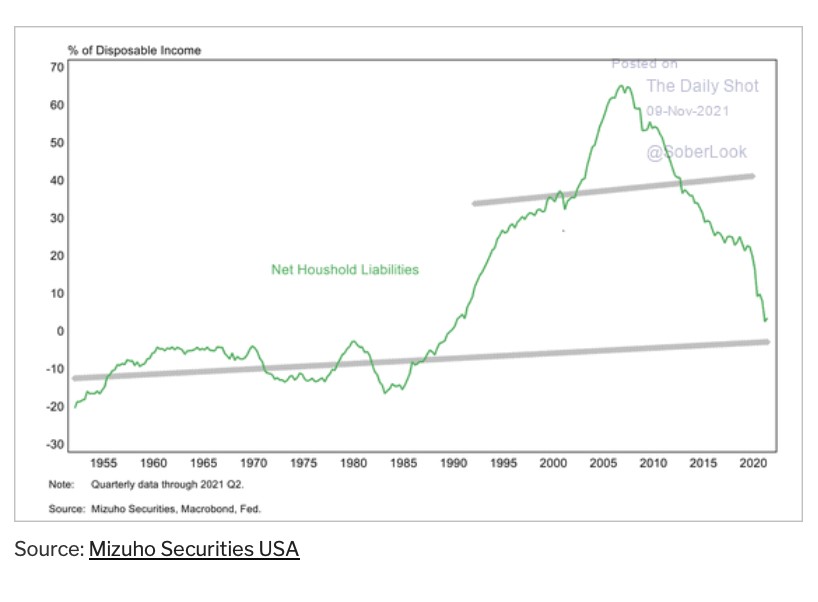

The U.S. Consumer Is Deleveraging

One thing is for sure; time and tide wait for no man, and most of the G7 world is getting older fast. Up to recently in the U.S., however, getting older did not mean you were retiring. In fact, many workers had to delay retirement plans because of the devastating losses they suffered in the 2000 Dot Com Bust and 2008 Great Recession.

The following chart from The Daily Shot shows the dramatic growth in the share of disposable income to net household liabilities from 1985 to 2009 and the significant de-leveraging since then:

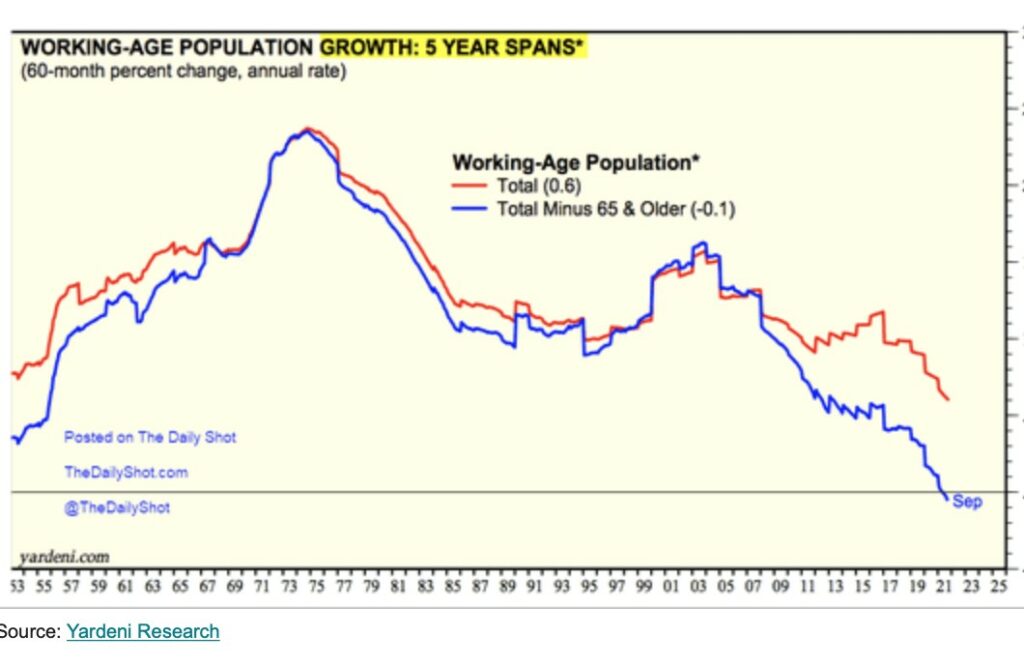

Covid-19 Solidified Retirement Plans

Covid-19 changed the employment mindset and now my cohort, the Baby Boomers, are retiring with no intention of ever working again. A number of experts suggest their exodus could mean 2.4 million fewer workers which is the projected gap between the blue line (proj.workers x 65+) and the red lines shown below:

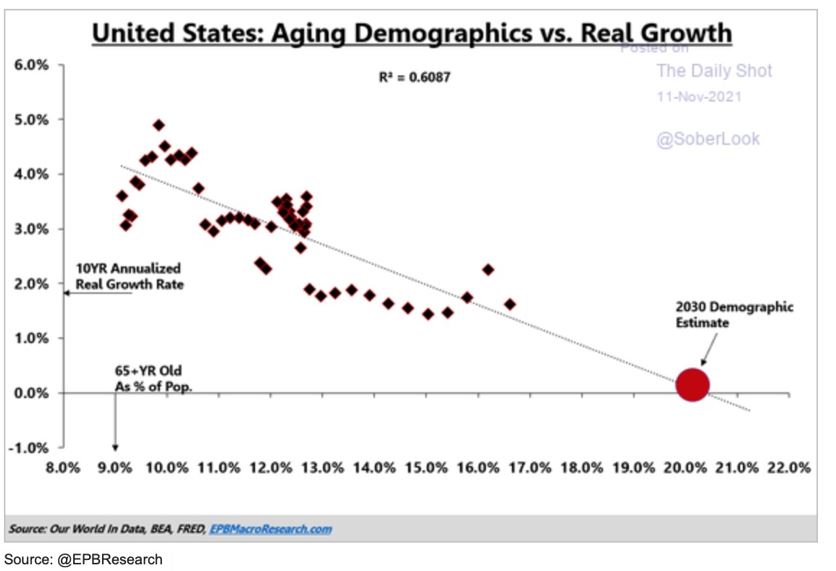

That was not the retirement trajectory anyone had projected before Covid-19 and now the relationship between employment and real GDP growth should be at the top of every conversation. The chart below projected it would be 2030 before aging demographics and retirement thinking meant 0% GDP growth. The current acceleration of that trend means we are almost there now.

I think it is logical to ask whether the permanent removal of 2.4 million workers can stunt real unit growth, but still inflate wages? If it is a possibility, there could be a difficult transition period where demand continues to exceed supply and workers’ wages rise, but units produced stay the same or even shrink.

Fed Can’t Beat Inflation This Time

I think they called this “stagflation” in the 1970’s and 1980’s, and it foreshadowed huge interest rate increases by Paul Volker to defeat inflation

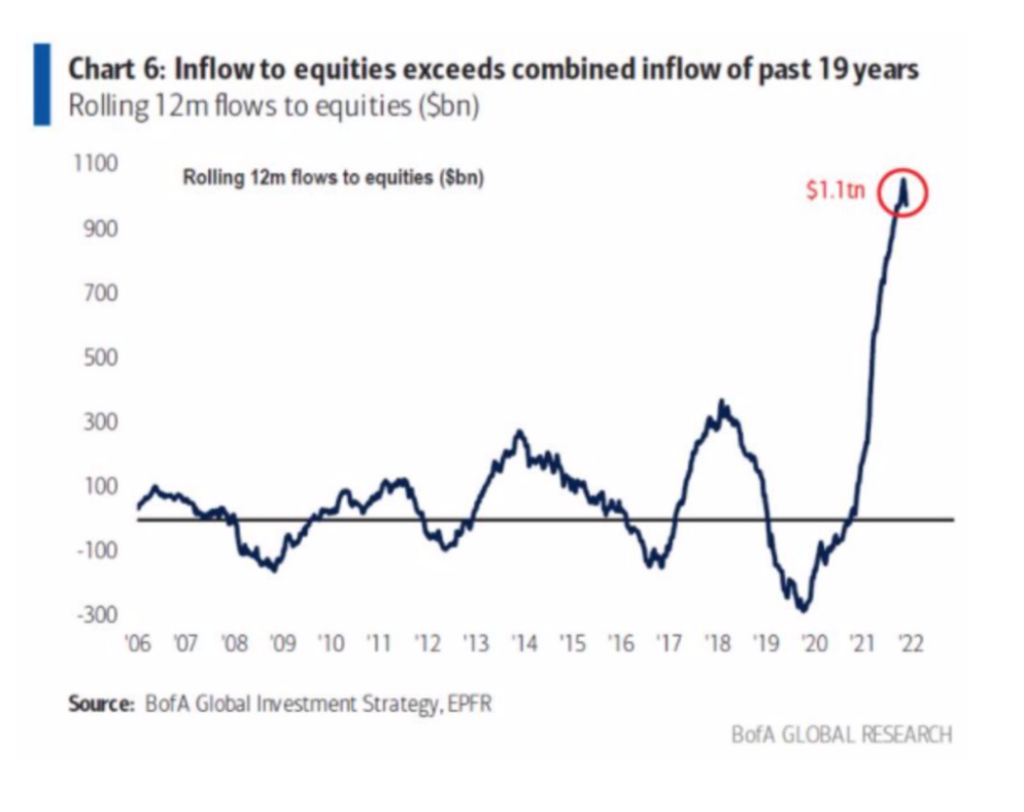

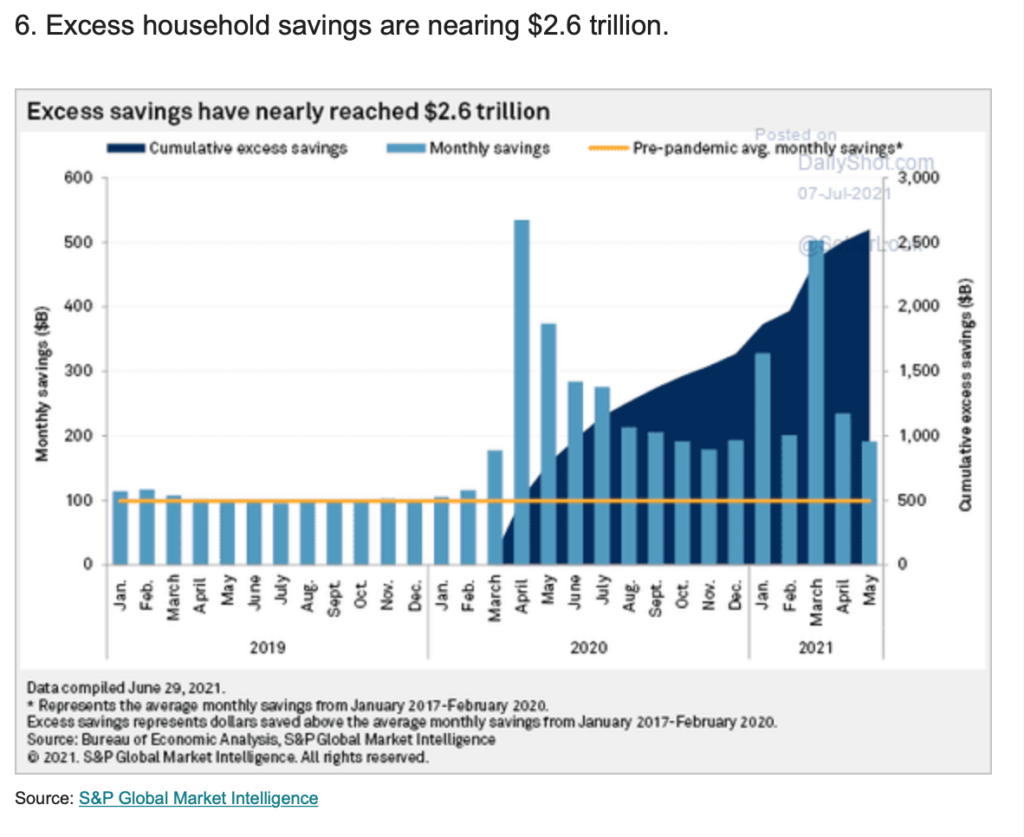

This time around that probably won’t happen as long as The Fed keeps financing government spending by monetizing the debt it is purchasing and also manages the yield curve through its highly active repo facility. But like water, demographics will find a natural course, and in the U.S. the early facts point to a committed group of oldsters who intend to save and invest, not spend. Here are two charts that suggest the enormity of their savings and investment.

The above commentary is for informational purposes only. Not intended as legal or investment advice or a recommendation of any particular security or strategy. Information prepared from third-party sources is believed to be reliable though its accuracy is not guaranteed. Opinions expressed in this commentary reflect subjective judgments based on conditions at the time of writing and are subject to change without notice.