Howard Marks, the founder of Oaktree Capital, is a prolific communicator. He has written letters to his investors since he began managing capital in the mid- 1980’s. While he started with a very stable asset class – corporate bonds – over time he moved into a much riskier neighborhood called “distressed debt” and high yield-aka “Junk Bonds”. He made that journey because he had evolved his investment skills to assess risk. The principal tenet of his early investment days was avoidance of loss. He believed winners would take care of themselves so he focused on balance sheets and cash flows to assess whether corporate bonds would pay interest and principal as promised.

Junk Bond Risk Assessment

In this new neighborhood where he was buying debt that was near default, or which had already defaulted, his ability to assess risk of loss was much murkier. There was the risk the issuer would declare bankruptcy and the rules of bankruptcy favored those investors who controlled a significant percentage of that class of debt. Bankruptcies also forced bond holders to become equity holders and sometimes led to debt holders having equity control. In the limbo period of a defaulted company’s reorganization there was also very little liquidity in the trading markets so your investments became bets you could not easily take back.

The one thing that was clear, however, was almost all the variables that could upend the good result were right in front of you. If you could intelligently work through all the possible ways, you could lose and ask whether the entry price you were paying for your position was discounted enough that you would make a profit even if many variables went against you, then the risk of loss was knowable.

Risk Assessment Changed With Central Bank Intrusion

This was before you had a third party with the power to print money emerge as a daily actor. Mr. Mark’s investment skills matter little if the Exogenous Actor (“EO”) with a bottomless checkbook is willing to buy into your asset class, or suddenly abandon it.

So, the manager skill moved from a Graham & Dodd “margin of safety” environment “what you know” to a Goldman Sachs “who you know in central authority” assessment of risk of non-payment. For the general investing public there also was a new confidence the Exogenous Actor would control financial panics and guarantee liquidity in all markets with the possible exception of Bitcoin, Game Stop and FTX , all of which were perceived as complete speculation.

The Exogenous Actor also created an investment climate that encouraged debt-based investment positions because it supplied liquidity and set interest rates and they got cheaper every year for almost 40 years. After 2008, there was always liquidity on demand for just about every asset class, especially after Covid- 19 measures to prevent market implosions.

Now as we look out at the “Sea Change” that Mr. Marks has written about and which I highlighted in my blog “Howard Marks Has New Advice For Investors”, the attitudes of the Exogenous Actor are harder to divine. Real inflation is affecting every corner of the world’s economy and it is particularly damaging to lower income groups as the costs of food, clothing, shelter, and transportation become 30- 50% more expensive than they were 3 years ago. This is a political problem that cannot be ignored and the EO has responded with surprising determination after bungling an early appraisal of inflation’s staying power.

However, an even larger problem is the world got hooked on low-cost debt as the engine of consumption. This was a wonderful multiplier of prosperity because all you needed was credit to buy-now-pay later. Multiple decades of prosperity got pulled forward especially into a concentrated period from 2010 to today.

So, as investors like Mr. Marks look at the investment landscape today, how do they compute margin of safety and loss avoidance? It is interesting that while they are looking back and remember the investment formula that worked from 1980 to 2020, they are predicting a “Sea Change” but not writing about their current ability to assess risk and avoid loss.

I think this may be the most important investment perspective for all of us amateurs. It is really hard to assess risk and avoid loss when you do not know all the rules and cannot predict how the Exogenous Actor will react. You can guess, and you can hope, but can you really know?

This is certainly a Sea Change, and I wonder whether there is any asset class that might be immune from a healthy discount for lack of visibility on how the EO will act?

A recent article on September 26 by “The Financial Times” titled “The Debt-Fueled Bet On US Treasuries That’s Scaring Regulators”, points out one dilemma. The EO has been an active overnight liquidity provider for the U.S. Treasury Market by loaning against Treasury Securities. This is allowing hedge funds to capture small irregularities in valuations by shorting the Treasury Markets. These hedge funds claim they are doing a good thing by providing liquidity to the bond market, when in fact it is the EO providing that liquidity. Here is a chart showing the recent popularity of buying Treasury Securities because of their perception of safety, and their yield which is 20x what an investor could obtain just 2 years ago. Notice that the long portion of the EO’s repo facility is now $2.5 Trillion up from $500 Billion just 13 years ago. Also, consider the massive risk to the bond market if the EO removes its support.

Consider that this caution flag applies to the safest corner of the investment neighborhood.

The rougher parts of town like the fixed income markets, and the equity markets, and all the alternative asset classes like hedge funds, private equity, and real estate are even more heavily influenced by how the EO is acting. All of these markets are also affected by inflation, are highly leveraged, and hooked on lower cost debt.

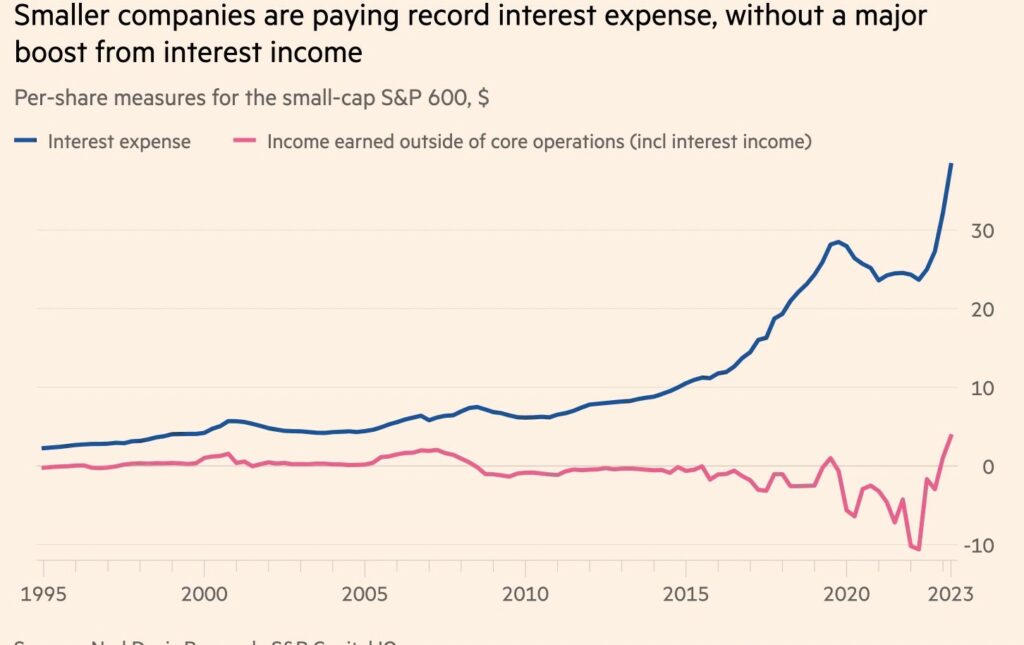

There is also a marked disparity between large and small companies. A recent article by the Financial Times, “US Small Cap Stocks Will Wilt in The Heat of Higher Interest Rates” written by Ethan Wu on September 26, claims almost 30% of NASDAQ stocks have floating rate capital structures versus just 9% for the S&P 500.

My conclusion about the Sea Change environment with an unpredictable EO is fourfold;

- Rogue Waves will be commonplace

- Investment strategies must be like good boats — you have to be able to get in and out of them easily and without discount for lack of marketability

- Swimming naked with large “net debt” exposures is drowning

- The EO is a political actor — it benefits those investors closest to it

The above commentary is for informational purposes only. Not intended as legal or investment advice or a recommendation of any particular security or strategy. Information prepared from third-party sources is believed to be reliable though its accuracy is not guaranteed. Opinions expressed in this commentary reflect subjective judgments based on conditions at the time of writing and are subject to change without notice.